What Is Stopping European Technological Innovation

... at least for now.

Hey, fellow Leader 🚀,

I am Artur, and welcome to my weekly newsletter. I am focusing on topics like IT Management, Innovation, and Leadership, with an Entrepreneurial mindset. My goal is to help you navigate the IT corporate landscape. Make better decisions, create awareness, and share real-world stories.

It has been a wild ride since I published the first article on the SoW. Exchanging views with you and hearing feedback on how these articles have been useful is what drives my motivation to write. Leave a comment, subscribe to the SoW, and be part of the community.

If this article resonates with you, or you know someone who might find it useful, just share the link!

There is significant political noise surrounding EU technological sovereignty. Among the perspectives shared online, there are valid concerns and realistic strategies, but also many irresponsible suggestions.

The Geopolitical and Market Landscape

The political relationship between the US and its European counterparts is becoming a bit tricky to manage. I won’t go into a full political analysis (as it is outside the scope of this SoW), but I want to share the context of the environment in which the EU is currently operating.

Technological Sovereignty is one of many topics currently under discussion in the EU’s political sphere, alongside other subjects like NATO and trade relations.

In practice, technological sovereignty is just another piece of a large geopolitical puzzle that European agents are trying to piece together. As a consequence, a movement has gained momentum in recent months encouraging European companies to rely more on domestic technological services.

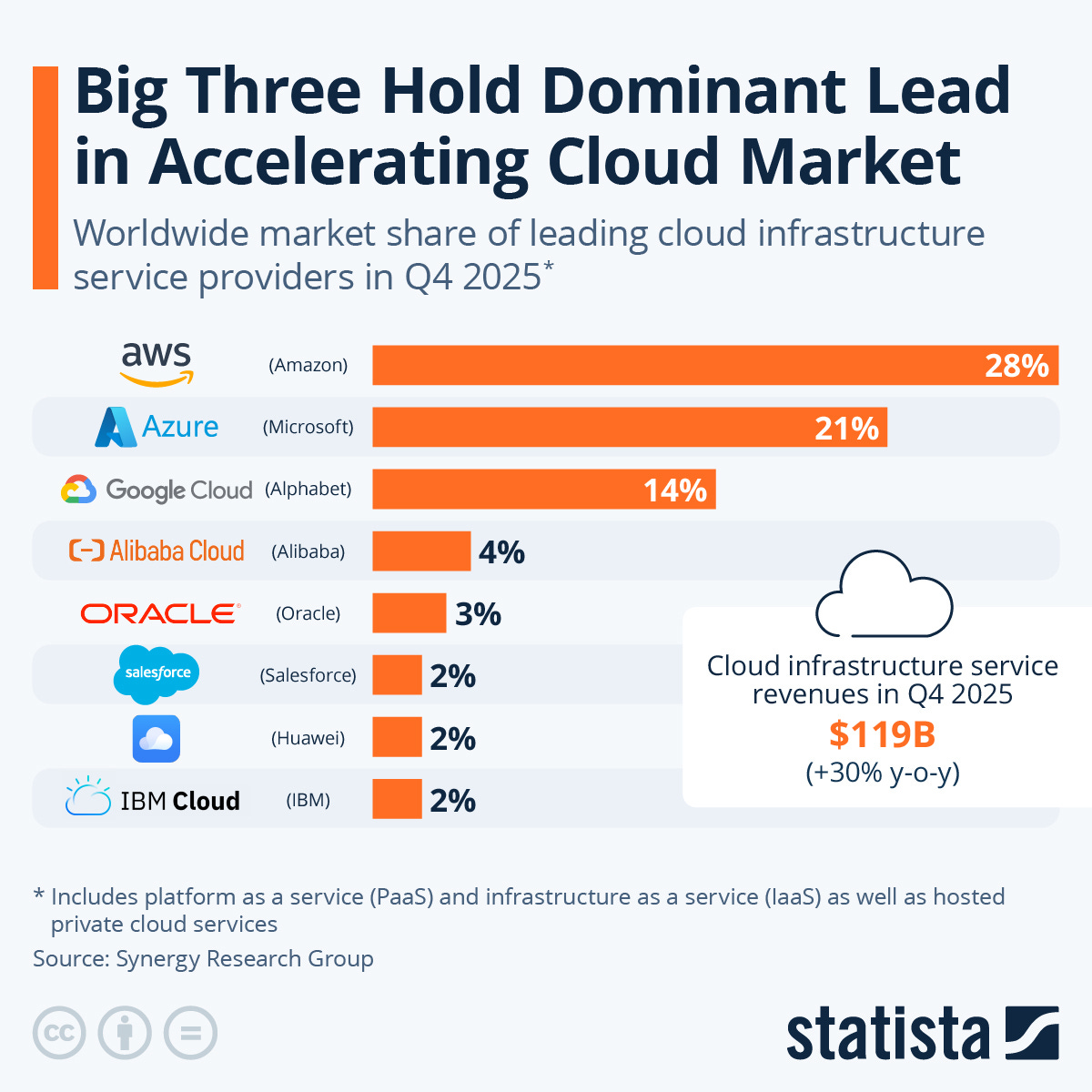

However, there is a catch: the majority of critical tech sectors are led by US-based companies. There is a specific reason for this, which I will cover shortly. To give an overview, in Cloud Services alone, AWS, GCP, and Azure (all US-based companies) account for more than 60% of the global market share.

There are virtually no European-based companies represented in the market share graphs.

If I were to attend an industry event in Central Europe and ask IT leaders to name a leading European provider, I bet the majority could only name one, and that company likely holds, at most, a 2% market share. Even then, people usually default to a provider from their own country. (I will leave a link here if you are curious about other European providers.)

A similar exercise can be performed with AI technology. From hardware to LLMs, there is very low market penetration by EU-based companies. As of the writing of this article, the most prominent European AI company is Mistral. But let’s be honest, when was the last time you actually used Mistral AI?

The Foundational Challenges

Currently, the EU faces two major foundational challenges that would require a massive restructuring.

Scale-up Money

When launching a startup, European entrepreneurs can only go so far using European capital.

They can develop a strategy and test products, but when a startup proves its model and needs to scale internationally (typically during Series C funding rounds), Europe fails to offer significant capital solutions. Consequently, entrepreneurs are often forced to look to the US, where they are frequently required to relocate their headquarters.

European countries often mirror this parochialism. If a domestic company wins a public project or receives state funding, a common requirement is to keep the build or the headquarters within that specific country. It is the same restrictive philosophy.

Is the EU lacking the capital to invest?

The reality is actually the opposite.

The European retail banking market is notoriously liquid. The majority of Europeans keep their money in traditional savings accounts rather than investing it (with a few exceptions, such as Sweden).

There is a deeply ingrained, conservative European mindset, and the banking system remains the primary source of corporate funding.

Even in universities, students are taught to build business plans for banks rather than for venture capital funds or private investors. Europe’s funding market requires a structural overhaul, yet this is unlikely to change in the near future.

Market Fragmentation

The second critical issue is European fragmentation.

If you establish a company in Belgium and wish to open a branch just a few kilometers away in Germany, you will encounter entirely different tax codes, administrative processes, and labor laws.

Despite the EU’s mandate for the free movement of people and services, its foundational core remains fragmented by decades of localized legislation. This creates significant hurdles for startups attempting to scale across borders. This fragmentation acts as a ‘tax on growth’ that entrepreneurs simply don’t have to pay in the US.

Doing business in the EU is inherently more difficult than in the US. While the US presents an equally competitive commercial market, it offers a unified regulatory framework that the EU simply cannot match.

The Solutions So Far

The European Union is well aware of these challenges and addresses them in the best way it can: through the launch of public European funds.

The EU’s main effort is to protect data sovereignty, and it maintains stricter GDPR concerns than either the US or China. The development of European AI data warehouses has become a strategic priority for the European Commission. While the availability of this capital is a positive step, it comes at the high cost of heavy bureaucracy.

Initiatives at the European level are primarily state-led. Despite their strategic importance, these projects can only go so far. A mature private sector, supported by alternative investment funds, would be faster and far more accessible from a bureaucratic standpoint.

Ultimately, a significant shift in mindset is required. Europe needs to move more capital into investment funds capable of fueling projects across all stages of growth (from initial seed money to late-stage scaling).

An Opportunity for the US

If US-based companies continue to secure their lead in the technological landscape, Europe will remain one of its primary technological trade partners. Conversely, if Europe manages to turn its technological competitiveness and legislative issues around, it could present an incredible opportunity for US investors.

Today, some US-based companies already maintain a percentage of their workforce in Eastern European countries. Without going into too much detail (a topic for a different article), if a developer in the US costs the company $250k annually (including all taxes and benefits), a developer with the same level of skills in Eastern Europe (like Poland or Romania) might cost around $60k (including all taxes and benefits). This represents a significant opportunity, especially for startups, as it allows for a larger team within the same cost baseline.

Another opportunity lies in the “mindset shock” (and this is where I am hoping for a true impact). Today, a US-based investor’s primary concern is growth, followed by profits.

In Europe, any business plan that cannot turn a profit by year two and achieve an ROI (Return on Investment) within four or five years barely stands a chance.

While the US has a significant market advantage, this mindset is the true “secret sauce” behind its technological lead. Europe would need to fundamentally shift its investment mentality to have any hope of gaining any form of technological lead.

That’s it. If you find this post useful, please share it with your friends or colleagues who might be interested in this topic. If you would like to see a different angle, suggest it in the comments or send me a message.

Cheers,

Artur